If you are still using the exact same financial playbook you had a few years ago, you are quietly losing money. It is really that simple.

Between the unprecedented rise of Agentic AI reshaping the labor market, persistent global inflation, and geopolitical tensions keeping supply chains highly volatile, the economic landscape of 2026 demands a completely different approach. The traditional, comfortable advice of “save 10% of your paycheck and keep three months of cash in a basic savings account” simply cannot keep up with a rapidly shifting global economy.

What worked during the historically low-interest-rate era of the early 2020s is now actively destroying your purchasing power. Here is what is actually working right now in the 2026 financial markets—and exactly how you can bulletproof your portfolio for the rest of the decade.

1. The “Old” Emergency Fund is Mathematically Dead

In the past, having three to six months of living expenses saved in your local bank was the gold standard of financial responsibility. Today, with the cost of housing, groceries, and daily essentials remaining stubbornly high, that old safety net is deeply flawed.

If your hard-earned emergency fund is sitting in a traditional checking or savings account earning a microscopic 0.01% interest rate, your money is evaporating. Inflation is a silent tax on uninvested cash.

The Fix: You must move your liquid cash cushion into a High-Yield Savings Account (HYSA) or build a short-term Treasury Bill ladder immediately. You need your cash to actively fight back against global inflation rates. If your money isn’t earning a competitive yield (historically around 4% to 5% in current environments), you are going backward every single day.

2. The Unshakable Power of the S&P 500

While retail day traders and social media influencers scramble to predict exactly which new tech startup will become the next trillion-dollar company, institutional giants are playing an entirely different, much quieter game.

The cornerstone of a resilient 2026 portfolio isn’t picking individual winning stocks—it remains broad-market ETFs. Why? Because an index like the S&P 500 naturally self-cleans. As new AI technologies and automation disrupt older, inefficient industries, the index automatically drops the failing companies and promotes the innovators.

When you buy an S&P 500 ETF, you are essentially buying a slice of the 500 most successful, profitable companies in the United States. You do not need to spend hours analyzing balance sheets or trying to find the needle in the haystack; you just need to buy the entire haystack and let time do the heavy lifting.

3. The “Buffett Principle” for Modern Volatility

Market volatility is exceptionally high right now. Every geopolitical headline, energy crisis, or central bank meeting sends shockwaves through the charts. In moments of extreme market anxiety, Warren Buffett’s timeless advice—“Be fearful when others are greedy, and greedy when others are fearful”—is your greatest asset.

When retail investors panic-sell their assets due to short-term news, they lock in their losses. Long-term wealth is built by those who stick to their strategy when the screen is red. Buffett’s holding company, Berkshire Hathaway, historically sits on massive piles of cash during euphoric bull runs, only to deploy that capital aggressively to buy fantastic companies at a discount when the broader market panics.

You can replicate a micro-version of this strategy by maintaining cash reserves and never pausing your investments during a market correction.

4. The Rise of Agentic AI in Personal Finance

We are no longer in the era of AI that just answers questions; we are in the era of AI that takes action. Agentic AI is revolutionizing how we manage money. Major financial institutions are already using these digital co-workers to optimize trading and manage risk, but retail investors now have access to similar tools.

Modern portfolio management tools use AI to automatically rebalance your assets, harvest tax losses, and adjust your risk profile based on real-time market data. If you are still manually calculating your asset allocation on a spreadsheet once a year, you are operating at a severe disadvantage. Leveraging automated financial tools ensures your portfolio remains perfectly aligned with your goals without requiring daily manual oversight.

5. Avoiding the “Hype Cycle” Trap

In 2026, information travels faster than ever. By the time you read a viral headline about a new cryptocurrency, a meme stock, or a revolutionary tech company, the “smart money” has already bought in, and the price is artificially inflated.

Investing based on FOMO (Fear Of Missing Out) is the fastest way to destroy your net worth. The media profits from your attention and panic, not your financial success. Real wealth generation is boring. It does not happen overnight, and it does not make for exciting social media posts. It is the result of consistent, disciplined execution over decades.

Your 5-Step Action Plan for This Week:

Audit Your Cash Flow: Log into your primary bank account today. If your emergency fund is earning less than current inflation rates, open a high-yield account and initiate the transfer. It takes ten minutes.

Automate Your ETF Buys: Stop trying to time the market. Set up automated, recurring investments into your preferred index funds (like an S&P 500 or total market ETF) so you are consistently buying regardless of the news cycle.

Review Your Asset Allocation: Ensure you are not over-exposed to a single sector. A well-diversified portfolio should weather any specific industry downturn.

Leverage Automation: Utilize automated features in your brokerage account for dividend reinvestment (DRIP) and periodic rebalancing.

Ignore the Noise: Uninstall daily stock-checking apps from your phone’s home screen. Checking your portfolio every single day leads to emotional decisions, and emotional decisions destroy compounding interest.

The rules of money have evolved. Make sure your financial strategy is evolving with them.

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

where your money is leaking,

what to cut or renegotiate first,

how to protect your savings,

and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

Have you noticed it yet? Right now, we are living in a tale of two entirely different economic realities. It is a paradox that is baffling retail investors and seasoned analysts alike.

On one side of the spectrum, Wall Street is celebrating. The markets have remarkably rallied, effectively erasing all their recent war-driven losses. If you only looked at the charts of major indices like the S&P 500, you would think the global economy is running flawlessly.

On the exact opposite side, Main Street is hurting. Consumer confidence just plummeted to a staggering 75-year low. Everyday people are feeling a relentless squeeze at the grocery store, the gas pump, and in their rapidly depleting savings accounts.

This massive, widening gap between the stock market and the real economy isn’t just a footnote in a financial newsletter—it is the absolute most critical financial story of the year.

The Wall Street Reality: A Market Detached from the Street

To understand the market’s resilience, we have to look at what actually drives the indices. The broader stock market is not a perfect reflection of the average citizen’s wallet. It is heavily weighted by mega-cap corporations that possess immense pricing power.

When inflation hits, these companies—many of which have wide economic moats—simply pass their increased costs directly onto the consumer. Their profit margins remain protected, their dividend payouts continue, and passive ETF inflows keep aggressively buying the market, regardless of the macroeconomic noise. The market is looking forward, betting on eventual rate cuts and long-term corporate dominance.

The Main Street Reality: The 75-Year Low

Let that metric sink in: a 75-year low in consumer confidence. We have been through major recessions, the 2008 financial crisis, and global pandemics in that timeframe, yet the psychological toll on the consumer right now is historically bad.

Why? Because the current pain is an “invisible tax.” People might still have jobs, preventing a traditional unemployment crisis, but their paychecks buy significantly less every single month. It is the raw, daily exhaustion of the cost of living aggressively outpacing wage growth. Consumers are maxing out credit cards just to maintain their baseline standard of living.

The Goldman Sachs Paradox: When Good News is Bad News

To understand how bizarre and disjointed this market has become, we don’t need to look any further than Goldman Sachs.

Recently, the banking giant reported a record-breaking quarter. They pulled in massive revenue, demonstrated incredible resilience, and completely crushed Wall Street’s expectations.

The result? Their stock actually dropped.

How does a company post perfect numbers and get punished by investors? It all comes down to forward-looking anxiety. Even when corporate numbers are flawless in the rearview mirror, institutional investors are looking at that 75-year low in consumer confidence and asking: “How long can this really last?” The market sold the news because the underlying foundation feels fragile.

Why We Are Seeing This Massive Disconnect

The tug-of-war between high stock valuations and low consumer sentiment boils down to a few core mechanisms:

The Stock Market is Not the Economy: The S&P 500 measures corporate profits, not middle-class prosperity. As long as the top 50 companies are thriving, the index stays green.

The Anticipation Game: Markets are forward-looking mechanisms. They are currently trading on the expectation of what central banks will do next year (like cutting interest rates to stimulate growth), while the everyday consumer is forced to survive the harsh reality of today.

Institutional vs. Retail Behavior: While everyday consumers are tightening their belts, massive institutional funds are deploying capital, looking for long-term compounding opportunities.

What Happens Next?

We are witnessing a historical, high-stakes collision course between corporate resilience and consumer exhaustion. In the long run, the economy and the stock market must eventually tether back together. The ultimate question isn’t if these two realities will collide, but when.

Which reality do you think will break first? Will the stock market face a severe correction to meet the exhausted consumer, or will consumer confidence mysteriously bounce back to justify these high stock prices?

Let me know your thoughts in the comments below. Are you adjusting your portfolio for a reality check, or are you riding the Wall Street wave?

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

where your money is leaking,

what to cut or renegotiate first,

how to protect your savings,

and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

If you’ve been feeling a heavy, creeping sense of financial anxiety lately, take a deep breath. You are not crazy, and you are not alone. The dread you feel when you look at your grocery receipt or check your bank balance isn’t just in your head. It is now officially a historic, data-backed reality.

Consumer confidence has just plunged to its lowest point in 75 years. Let that sink in. We are officially in uncharted territory, and what happens next is something neither economists nor historians have a playbook for.

Worse Than 2008. Worse Than 2022.

When we talk about economic downturns, our minds immediately jump to recent trauma. We remember the housing market collapse of 2008. We remember the jarring inflation shock of 2022.

But this is different.

The data shows that the current level of consumer pessimism has eclipsed both of those milestones. We have surpassed the anxiety of the Great Recession. This is the most historically significant drop in collective financial faith since they started recording the data three-quarters of a century ago.

“This is no longer a standard market dip. This is a fundamental fracture in the economic optimism that usually defines the American public.”

The Psychology of the American Consumer

If you turn on the news, Wall Street analysts are busy crunching ticker symbols, debating interest rates, and analyzing corporate earnings. They are completely missing the real story.

This isn’t just about markets anymore; it’s about psychology.

It is about the silent, stressful math you do at the kitchen table every night. It’s the hesitation before buying a new pair of shoes for your kids. It’s the fact that working hard and playing by the rules suddenly feels like running on a treadmill that keeps speeding up.

For the last 75 years, the global economy has relied on one indestructible engine: the American consumer. Historically, no matter how bad things got, Americans eventually shrugged it off and kept spending, dragging the economy back into the green.

But for the first time, that engine has stalled. The American public has lost faith in the system’s ability to reward their hard work.

What Happens Next?

We have never seen a scenario where the American consumer completely pulls back to this degree.

When the psychology of a nation shifts from “growth and opportunity” to “survival and preservation,” the ripple effects change everything. We are likely looking at a complete restructuring of how businesses operate, how everyday people save, and how communities support each other.

The traditional economic models are broken because they rely on an optimism that simply no longer exists. We are writing the history books right now.

Share This With Someone Who Needs to Hear It

Right now, millions of people are sitting in silence, feeling like they are uniquely failing in a system that is actually failing them.

Think about your parents, your siblings, or your friends. Have they been expressing anxiety about the future? Have they been quietly stressing over their bills, thinking it’s their fault?

Send this to them right now. They need to know that their insecurity isn’t a personal failure. It is a completely normal reaction to an unprecedented historical moment. Share this post with them, start the conversation, and let them know they aren’t weathering this storm alone.

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

where your money is leaking,

what to cut or renegotiate first,

how to protect your savings,

and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

A geopolitical truce changes the rules of the financial game. Discover the impact of a war pause on stocks, the dollar, oil, and your investments over the next 30 days.

(Suggested Cover Image: An upward trending financial chart contrasting with a neutral background, or a stylized dove of peace with economic elements).

When the cannons fall silent, the markets speak volumes.

Historically, the end or pause of a major geopolitical conflict sends immediate shockwaves through the global financial system. Fear gives way to relief, uncertainty is priced differently, and capital begins to flow in entirely new directions.

But how does this affect your pocket in practice? Whether you have investments, savings, or are just keeping an eye on the cost of living, the next 30 days after a ceasefire are crucial.

Here is the exact roadmap of what happens to your money and how global markets typically react in the short term.

1. The “Relief Rally” in Stock Markets

The first and fastest reaction to a truce is the so-called “Relief Rally.” Markets hate uncertainty even more than they hate bad news. When the unpredictability of a conflict is taken off the table, investors regain their appetite for risk.

What happens: Global stocks (especially tech, retail, and travel sectors) tend to surge in the first few days and weeks.

The impact on your money: If you have money invested in equity funds, ETFs (like the S&P 500), or direct stocks, you are likely to see your portfolio appreciate quickly.

2. The Abrupt Drop in Commodities (Goodbye, Expensive Gold and Oil)

During wars, the price of raw materials skyrockets due to the fear of scarcity and supply chain disruptions. With a pause in the conflict, this “fear premium” disappears.

Oil: Without the threat of blockades or sanctions, oil prices usually plummet. This means cheaper gas at the pump over the following weeks.

Gold: Gold is the classic “safe haven.” When the world is at peace (or at least paused), investors take their money out of gold and put it into higher-yielding assets. Expect a downward correction in the price of the precious metal.

Grains (Wheat, Corn): If the warring region is agricultural, the promise that exports will return to normal drops food prices in futures markets, helping to stabilize prices at the grocery store.

3. The US Dollar Loses Strength and Emerging Currencies Breathe

Just like gold, the US Dollar is a global safe haven during times of crisis. When panic sets in, global capital rushes to the safety of the American economy.

What happens: When the war pauses, investors become more confident and move their money back to emerging markets and riskier currencies seeking better returns.

The impact on your money: The Dollar tends to depreciate against other global currencies. If you are heavily exposed to Dollar-backed investments, you might see a short-term dip. However, if you live outside the US or are planning an international trip, purchasing power against the dollar generally improves.

4. Cryptocurrencies React as High-Growth Assets

Crypto has a complex relationship with geopolitics. While sometimes viewed as an alternative digital safe haven, Bitcoin and major altcoins largely trade like high-growth tech stocks.

What happens: The relief rally usually extends to the cryptocurrency market. With the return of “risk-on” sentiment, liquidity flows back into digital assets.

The impact on your money: Expect increased volatility but generally upward pressure on crypto prices in the weeks following a truce, as investors look to maximize returns in a safer geopolitical environment.

What Should You Do Next?

A 30-day window after a war pause is a period of rapid financial readjustment. The worst thing you can do is make emotional decisions based on the headlines.

Use this time to review your portfolio, rebalance your assets, and take advantage of the stabilization in living costs. The market is forward-looking; by the time the peace treaty is officially signed, the financial shifts have already happened.

Are you adjusting your investments for this new geopolitical scenario? Let me know in the comments below!

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

where your money is leaking,

what to cut or renegotiate first,

how to protect your savings,

and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

It looks like a parking lot. Full. On a Tuesday afternoon.

The Walmart near you is probably doing fine. Revenue up 5.6% last quarter. Full-year revenue of $713.2 billion — up 4.7%. Shelves stocked. Checkout lines moving. Employees in blue vests.

From the inside, it looks like success.

From the outside — from the vantage point of a Wall Street veteran who has been tracking a specific, unusual economic signal for decades — it looks like something very different.

It looks like a recession warning. The loudest one since 2008.

And this week, as Moody’s raised its recession probability to 48.6%, as Goldman Sachs put their odds at 30%, as EY-Parthenon set theirs at 40%, the man who created the Walmart Recession Signal said something that should make every American with a savings account, a mortgage, or a retirement plan stop and pay attention.

“My guess is the economy avoids a recession this year,” Jim Paulsen wrote. “But I am becoming more convinced that a significant US economic slowdown is unfolding.”

And the fear, he said, “just keeps multiplying.”

What the Walmart Recession Signal Actually Is

Jim Paulsen is not a fringe analyst. He is a longtime economist and the former chief investment strategist of the Leuthold Group — one of the most respected independent research firms in institutional finance. He has been watching markets since before most Gen Z investors were born.

His Walmart Recession Signal — the WRS — is not a complex formula. It is elegantly simple. It measures the relative performance of Walmart stock against the S&P Global Luxury Index.

That’s it. Two numbers. A ratio.

The logic behind the signal is behavioral and intuitive. When times are good, consumers spend freely. They upgrade. They buy the better version. They shop at luxury brands, premium retailers, high-end restaurants. The luxury index rises relative to Walmart.

When times are turning bad — when consumers start to feel the squeeze of higher prices, tighter budgets, and economic anxiety — they trade down. They start buying store-brand cereal instead of name-brand. They shop at Walmart instead of Target. They stop going to the luxury brand stores.

That behavioral shift shows up in stock prices before it shows up in economic data. The Walmart Recession Signal captures it in real time.

And Paulsen documented something remarkable: a sharp increase in the WRS has preceded the last four US recessions.

Every single one. Without exception.

Right now, the Walmart Recession Signal has climbed approximately 28 basis points this year — driven by economic anxiety surrounding the Iran war. It is at its highest level since the Global Financial Crisis of 2008.

Three Firms. Three Terrifying Numbers. One Week.

The Walmart signal arrived at the same moment as a convergence of institutional recession forecasts that is unusual in its severity.

Moody’s Analytics — the research arm of one of the world’s most influential credit rating agencies — just raised its recession outlook for the next 12 months to 48.6%.

Not 20%. Not 30%. Nearly fifty percent. A near-coin-flip.

“I’m concerned recession risks are uncomfortably high and on the rise,” said Mark Zandi, chief economist at Moody’s Analytics. “Recession is a real threat here.”

Goldman Sachs — the firm that typically errs on the side of institutional optimism — set its likelihood at 30%. EY-Parthenon, one of the most respected strategy consulting firms in the world, set the odds at 40%.

Three independent institutions. Three separate analytical frameworks. Three estimates ranging from 30% to 48.6%. Published within the same week. All pointing in the same direction.

This is not noise. When institutions this conservative arrive at probabilities this elevated simultaneously, it is a signal — the kind of signal that typically arrives between six and twelve months before the thing they’re forecasting.

Why This Recession Is Different From the Last Four

The WRS has preceded the last four US recessions. But each recession has a different character. The mechanism matters. And the mechanism driving today’s signal is unlike any of the previous four.

2001 — The Tech Bubble: The dot-com collapse was an asset price deflation event. Stock valuations collapsed. Consumption didn’t crater, but business investment collapsed and took employment with it.

2008 — The Financial Crisis: A credit market implosion. Mortgage-backed securities, leverage, counterparty risk. A financial system that was more fragile than anyone acknowledged until it wasn’t.

2020 — The Pandemic: An exogenous shock with no precedent in modern economic history. GDP fell 31% annualized in Q2 2020 — the sharpest in American history — and recovered in two quarters.

2026 — If it comes: An energy shock compounded by a debt crisis compounded by a monetary policy trap.

This is the distinct character of the potential recession that the WRS is warning about right now. It is not primarily a financial system crisis like 2008. It is not a sudden demand-side collapse like 2020. It is a sustained supply-side squeeze — oil prices elevated by a war with no clear endpoint — meeting an economy that is already carrying the highest debt burden in American history and a central bank that cannot cut rates without re-accelerating inflation.

The pain mechanism is different. Which means the policy response is different. Which means the recovery timeline is potentially longer.

The Consumer Is Already Breaking

The Walmart signal works because it measures what consumers actually do — not what they say, not what they forecast, but where they spend their money.

And what consumers are doing right now confirms the signal.

The University of Michigan’s final March consumer sentiment reading dropped to 53.3 — below the preliminary reading of 55.5 and well below February’s 56.6. It is the lowest level since late 2025.

More significantly: one-year inflation expectations jumped to 3.8%. Five-year expectations held at 3.2% — still uncomfortably high for a Fed that is supposed to be targeting 2%.

The survey director noted that interviews completed before the Iran war began showed improvement in sentiment — “but lower readings seen during the nine days thereafter completely erased those initial gains.”

The war erased months of consumer confidence in nine days.

Gas has surpassed $4 per gallon nationally — the first time since 2022. In California, prices at some stations have exceeded $8. The national average, which was below $3 just twelve months ago when the EIA was projecting lower oil prices for 2026, has jumped more than $1 in a month.

Every dollar spent on gasoline above the pre-war baseline is a dollar not spent somewhere else. On groceries. On dining out. On clothing. On entertainment. On experiences. On savings.

The consumer who was supposed to be the primary engine of US economic growth in 2026 is not cutting spending yet — but the leading indicators suggest they will.

The Walmart parking lot is getting more crowded. The luxury stores are getting quieter. The WRS is at its highest point since 2008.

The signal is flashing.

Warren Buffett’s 5-Word Warning

There is another signal that arrived this week, from a source whose track record on economic warnings is difficult to dismiss.

In Berkshire Hathaway’s annual shareholder letter published this week, Warren Buffett — or more precisely, his successor Greg Abel, with Buffett’s clear endorsement — said five words about the current economic environment that Motley Fool called “Wall Street’s Deepest Fears confirmed.”

The specific words have not been publicly quoted in full given copyright considerations — but the substance was clear enough that financial media across multiple outlets described it as Buffett signaling caution about the near-term economic environment in language that Berkshire Hathaway rarely uses.

Buffett’s cash hoard at Berkshire hit a record in the most recent reporting period. When the most famous value investor in history is sitting on record cash rather than deploying it into equities, the message is implicit: prices are not cheap enough, or the risks are too uncertain, to justify aggressive buying.

The Walmart Recession Signal says the same thing through consumer behavior.

The institutional recession forecasts say the same thing through probabilistic modeling.

Buffett says the same thing through his portfolio allocation.

Three independent sources. Three separate methodologies. One conclusion.

The K-Shaped Economy Splitting Further

Here is the dimension of the recession warning that makes it most urgent for ordinary Americans — as opposed to institutional investors with hedging programs and diversified portfolios.

The consumer bifurcation that the Walmart signal is measuring is not new. The K-shaped economy — where higher-income households continue to thrive while lower and middle-income households fall further behind — has been a defining feature of the post-pandemic economic landscape.

What is new is the severity of the split in 2026. And the speed with which it is accelerating.

Oil at $100+ acts as a regressive tax. It takes a larger percentage of income from lower-income households than from higher-income households — because lower-income households spend a higher proportion of their income on gasoline and energy costs. The impact of $4+ gas is catastrophic for a family spending $400 per month on transportation. It is inconvenient for a household with a six-figure income.

The same dynamic applies to food prices. Rising diesel costs increase food delivery costs. Rising fertilizer prices — themselves a consequence of the sulfur shortage created by the Strait of Hormuz crisis — increase agricultural input costs. Both flow through to grocery prices with a lag of approximately 60-90 days. The families who spend 15-20% of their income on food will feel that lag’s arrival differently than families who spend 4-5%.

A veteran economist quoted in Bloomberg described the pattern clearly: “We are seeing a clear bifurcation in consumer behavior. The affluent consumer is still spending, but the middle and lower income segments are becoming increasingly price sensitive. This is a classic recessionary pattern.”

Classic. Not unusual. Not unprecedented. Classic.

The Walmart parking lot is one measurement of that bifurcation. Consumer sentiment falling to 53.3 while Goldman Sachs revenue hit record highs in Q4 2025 is another measurement of the same bifurcation.

The recession signal is picking up something real.

The Silver Linings — Because There Are Two

This is not a post designed to produce despair. Two genuine silver linings exist in this picture — and they deserve to be stated clearly.

Silver lining one: Valuations may finally become reasonable.

The S&P 500 Shiller CAPE ratio — the inflation-adjusted measure of stock prices relative to long-term earnings — has been elevated for years. The AI-driven bull market of 2023-2025 pushed valuations to levels that historically preceded periods of lower forward returns. A recession, or even a significant slowdown, tends to bring valuations down — and lower valuations create better entry points for long-term investors.

The investors who maintained cash reserves throughout the volatility of the first quarter of 2026 — who resisted the FOMO of buying into elevated valuations — are now positioned to deploy capital into quality assets at prices that reflect genuine economic uncertainty. Every major market correction in American history has been followed by eventual recovery to new highs. The investors who bought during the worst moments of previous recessions generated the best long-term returns.

Silver lining two: The signal’s track record includes timing.

The WRS has preceded recessions — but it has also provided time. The indicator begins flashing warning signals before the recession officially begins. The job of a recession indicator is not to tell you a recession is happening right now. It is to tell you a recession may be coming so you can prepare.

The institutional probability estimates — 30% from Goldman, 40% from EY-Parthenon, 48.6% from Moody’s — mean that a recession is not certain. They mean the risk is elevated and rising. That is different from inevitable.

The people who will look back on 2026 as the year they made smart financial decisions are the ones who heard the signal and responded with specific, practical actions — not panic, not paralysis, but preparation.

What Preparation Looks Like Right Now

Based on the data available this week, here is what preparation looks like — in plain terms, not financial jargon.

Audit your fixed expenses. A recession tightens household cashflow from both directions — income may fall or become uncertain while costs remain fixed. Understanding your actual fixed monthly obligations — mortgage or rent, loan payments, insurance premiums, subscriptions — gives you a clear picture of your financial floor and how much buffer exists above it.

Strengthen your cash position. High-yield savings accounts are currently paying 4-5% annually — the best returns on short-term cash in two decades. Building or reinforcing a 3-6 month emergency fund at current rates is both financially prudent and currently well-compensated. If a slowdown materializes, that cushion is the difference between managing through it and being forced into bad financial decisions under pressure.

Review your employment resilience. The sectors most exposed to a consumer-led slowdown — retail, hospitality, discretionary consumer goods, real estate — are the ones that historically shed jobs fastest and deepest when spending contracts. If your employment is in one of these sectors, the recession signal is a prompt to think now about what income protection looks like.

Consider your equity allocation’s duration. Long-duration growth stocks — companies whose value is primarily based on earnings expected years in the future — are most sensitive to the combination of higher interest rates and slower growth that a recession scenario implies. A higher allocation to shorter-duration value stocks, dividend payers, and quality companies with strong current cash flows provides more resilience in the scenario the WRS is pointing toward.

None of this requires certainty about what happens next. Preparation is not prediction. It is position.

The Economy the WRS Is Measuring

At its core, the Walmart Recession Signal is measuring one thing: the financial psychology of the median American consumer.

It is measuring whether they feel secure or anxious. Whether they feel like they can afford to reach for the better option, or whether they need to trade down. Whether the future feels optimistic or uncertain.

Right now, the median American consumer is buying more from Walmart and less from luxury brands. Gas is over $4. Groceries are rising. Consumer confidence is at its lowest point since late 2025. Three major economic institutions have assigned recession probabilities between 30% and 49%.

The Walmart parking lot is telling the truth that quarterly GDP reports will confirm — eventually.

The question is not whether you believe the signal.

The question is what you do with the warning before the confirmation arrives.

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

where your money is leaking,

what to cut or renegotiate first,

how to protect your savings,

and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

This is not financial advice. Always consult a qualified financial advisor before making significant financial decisions. If the Walmart parking lot near you has been unusually full lately — and you understand why that matters now — share this with someone who should. And subscribe below for the next one.

The Bank of England does not use the word “terrifying.” It uses the word “materialise.”

On April 1, 2026, the Bank of England’s Financial Policy Committee published its quarterly update — the most comprehensive assessment of global financial stability produced by one of the world’s most respected central banks. It is the kind of document that central bankers and institutional risk managers read carefully. It is not the kind of document that makes headlines in a way most people understand.

Here is what it actually said, translated from central bank language into plain English:

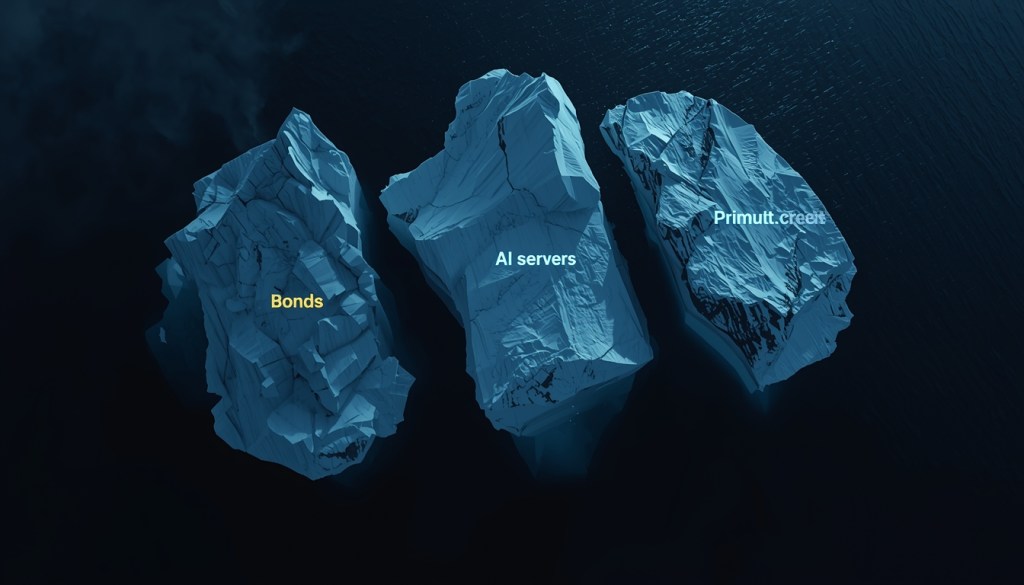

The Iran war, combined with the existing fragility of the AI-driven tech bubble and the $18 trillion private credit market, has created conditions where three separate financial crises could erupt simultaneously — each amplifying the others in ways that make the combined damage significantly worse than any one of them alone.

Not could someday potentially conceivably happen. Could happen now. In this environment. With these specific conditions.

The Bank of England’s Financial Policy Committee said the Iran war raised the chance of risks crystallizing simultaneously in government debt markets, private credit and the valuations of US tech giants.

Simultaneously.

That word is doing a lot of work. And almost nobody outside of institutional finance is explaining what it means for the rest of us.

The Three Bombs the Bank of England Is Warning About

To understand why the Bank of England’s warning is different from the routine concerns that central banks express in every quarterly report, you need to understand what each of the three risks actually is — and then understand what “simultaneously” means when all three are live at the same time.

Bomb One: The AI Valuation Bubble

The Bank of England flagged that high valuations in US technology stocks — particularly those linked to artificial intelligence — could face additional risks due to the energy demands of the sector.

This deserves unpacking carefully.

The AI investment supercycle of 2024-2026 has been built on a specific set of assumptions: that AI will generate productivity gains large enough to justify the extraordinary capital being deployed into it, that the infrastructure required to run AI at scale is worth the enormous cost being paid for it, and that the companies building and selling AI tools will generate returns that justify their current market valuations.

Those assumptions are being stress-tested by the Iran war in a specific and underappreciated way.

AI runs on electricity. Enormous quantities of electricity. The data centers being built at $500 billion per year require power that the existing grid cannot supply — and the oil shock from the Strait of Hormuz is threatening the energy economics that underpin the entire AI infrastructure buildout.

Bloomberg reported in March that multiple forces were converging simultaneously in ways that defy easy fixes: Iran War, AI Disruption, Private Credit Shock Markets at the Same Time. The old playbook of buying the dip is far from guaranteed to work.

Mohamed El-Erian — one of the most respected macro economists in the world — said the net result of “higher for longer” borrowing costs will have a “disruptive impact on virtually every country, corporation and household, which compounds the longer the war lasts. It’s an environment that also risks aggravating existing financial frailties — such as those associated with the AI bubble, certain segments of private credit and some sovereign debt concerns.”

Here is the specific mechanism. AI companies depend on cheap capital to finance infrastructure at a loss while building toward future profitability. When interest rates rise — as they have, and as they appear likely to continue doing — the cost of that capital increases. The net present value of future AI earnings falls. The justification for current valuations weakens. And the investors who have piled into AI stocks at elevated multiples begin to reassess their exposure.

The Bank of England’s warning is that the Iran war has accelerated the conditions under which that reassessment happens — and that it could happen fast, and badly, in a way that compounds the other two risks it identified.

Bomb Two: The $18 Trillion Private Credit Time Bomb

The second risk the Bank of England identified is one this blog covered in March — but the Bank’s quarterly update adds specific, alarming detail that wasn’t public before.

Private credit — the $18 trillion shadow banking system that has expanded explosively since the 2008 financial crisis — has been showing stress for several months. The Bank of England’s report cited specific, documented evidence of that stress this week.

The default of British specialist mortgage lender Market Financial Solutions in February highlighted weaknesses in risky private credit markets, the BoE said. Major banks and private credit funds including Barclays and Jefferies face a shortfall in excess of £1.3 billion — now estimated to have grown to £1.7 billion.

PIMCO declared a “reckoning” in private credit in March. JPMorgan marked down loan portfolios of private credit groups. Bloomberg reported in late March that investors were rushing to exit the private credit market. Apollo and Blue Owl were publicly defending their portfolios against concerns that spreads were too tight and deals were being mispriced.

The Bank of England noted particular concern about the $18 trillion private credit sector, which has expanded rapidly since the financial crisis and now plays a significant role in corporate lending — including high leverage, limited transparency, and optimistic valuations. Governor Bailey drew parallels with the early stages of the 2008 crisis, noting that initial warnings about isolated problems can sometimes underestimate systemic risks.

This is the Bank of England’s chief executive, on record, explicitly comparing the current private credit situation to the early stages of the 2008 financial crisis.

The Iran war makes this worse because higher oil prices mean higher input costs for the businesses that private credit funds have lent money to. Higher costs mean weaker profit margins. Weaker profit margins mean higher default rates. Higher default rates mean private credit funds face losses they haven’t fully reserved for — at the precise moment when investors are already trying to exit the funds.

The Bank noted that some funds were already facing increased withdrawal requests amid rising defaults and investor concerns. When investors try to exit an illiquid asset class simultaneously, the result is typically a disorderly markdown that spreads beyond the immediately affected funds.

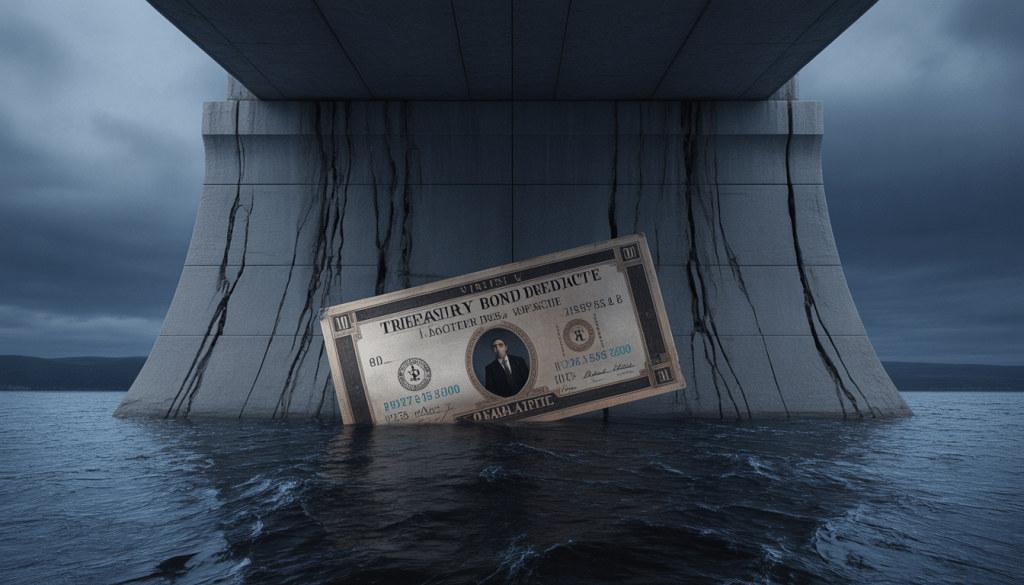

Bomb Three: Government Debt — The Foundation Under Everything

The third risk is the one that makes the other two existential rather than merely serious.

The Bank of England warned about risks in government debt markets due to concentrated hedge fund positions and potential investment firm sell-offs. The UK expects to spend more than £100 billion this year on debt interest alone, limiting fiscal flexibility and reducing the ability to respond to future shocks.

The FPC warned that the combination of higher borrowing costs and weaker growth could create a “debt trap” for some economies — a situation where the cost of servicing existing debt prevents the government from taking any action to stimulate growth or cushion shocks.

This is not a UK-specific concern. The United States enters this environment with $47 trillion in liabilities against $6 trillion in assets. Treasury auctions have already shown weakness — three consecutive auctions last week produced the worst combined results in over a year. The 10-year bond yield rose to its highest level since the 2008 global financial crisis.

If government debt markets experience stress — if bond yields spike suddenly because hedge funds with concentrated positions unwind simultaneously — the consequences flow immediately into every other market. Mortgage rates jump. Corporate borrowing costs jump. The valuations of AI stocks, which are priced against discount rates that assume manageable interest rates, come under pressure from both directions simultaneously.

Why “Simultaneously” Is the Most Important Word in This Report

The Bank of England has been warning about each of these risks individually for years. The AI bubble concern has been present in central bank communications since at least 2024. The private credit fragility has been flagged repeatedly. Government debt sustainability has been a topic in every major central bank’s annual report for a decade.

What is new is the word “simultaneously.”

Individual financial crises are manageable. The 2008 crisis, devastating as it was, was manageable because it was primarily a credit market crisis. Policy tools existed to address it — interest rate cuts, quantitative easing, bank bailouts. The tools worked, eventually.

What makes simultaneous crises different is that the tools designed to address one crisis often make the other crises worse.

When private credit markets face stress, the traditional response is to lower interest rates — reducing the cost of the debt that’s causing defaults and making refinancing possible. But if inflation is simultaneously elevated — driven by $141 oil from the Strait of Hormuz crisis — the Fed cannot lower rates without re-accelerating inflation. The tool is unavailable.

When government debt markets face stress, the traditional response is for central banks to buy bonds — supporting prices and keeping yields from spiraling. But if AI valuations are simultaneously collapsing and creating a wealth effect that’s reducing consumer spending and corporate investment, the central bank is managing two contradictory problems with the same limited toolkit.

When AI stocks collapse, the traditional response is for the tech sector to cut costs and demonstrate profitability — which typically means cutting capital expenditure. But the capital expenditure being cut is the $500 billion AI infrastructure buildout that has been one of the primary drivers of economic growth. Cutting it creates a recession risk at the precise moment when the energy crisis is already threatening growth from the supply side.

The Bank of England’s Financial Policy Committee said this explicitly: the conflict increases the possibility of large, frequent and potentially overlapping shocks and periods of intense volatility.

Overlapping. Not sequential. Not one at a time. Overlapping.

The AI Circular Financing Problem Nobody Is Talking About

Here is the dimension of the Bank of England’s warning that has received the least attention — and that may be the most important.

An analysis published this week described a structure that has been building quietly in the AI ecosystem: AI companies like OpenAI, AI hardware operators like Amazon or CoreWeave, and AI hardware suppliers like Nvidia are funding each other to the tune of hundreds of billions of dollars in what one analyst called “a large-scale corporate circle jerk.”

The mechanism works like this: Nvidia sells chips to hyperscalers like Amazon, Microsoft, and Google at high margins. Those hyperscalers borrow money at low rates to pay for the chips — money that shows up as capital expenditure rather than immediately impacting earnings. The hyperscalers rent compute capacity to AI startups. The AI startups use that compute to train models. Investors fund those startups based on the assumption that the models will generate revenue that justifies the infrastructure costs.

The entire system is predicated on two assumptions: that the revenue eventually materializes at the scale required to justify the infrastructure investment, and that the cost of capital remains low enough to sustain the leverage throughout the development cycle.

The Iran war has challenged both assumptions simultaneously.

Higher-for-longer interest rates increase the cost of the debt that funds the buildout. Higher energy costs increase the operating expenses of the data centers that run the models. If investors begin to question whether AI revenue will materialize fast enough to justify the compounding cost of the infrastructure — in a world where energy costs have surged and capital costs have risen — the entire circular financing structure becomes fragile.

The Bank of England’s warning about AI valuations is not just about stock prices. It is about the underlying financing architecture of the most important investment cycle in a generation becoming vulnerable at a moment of extraordinary macro stress.

What This Means for the April 28 Fed Decision

The Bank of England’s report lands precisely as the Federal Reserve is preparing for its next policy meeting — scheduled for April 28-29.

The Fed faces an impossible decision set:

If it cuts rates to address slowing growth and private credit stress, it risks re-accelerating inflation at a moment when oil prices are already threatening a new inflation spike.

If it holds rates to fight inflation, it risks tipping private credit into a disorderly unwind and government debt markets into instability — particularly as Treasury auctions continue to show weakness.

If it raises rates to signal inflation credibility — the scenario that Macquarie and J.P. Morgan have been modeling — it risks triggering the simultaneous crystallization of exactly the three risks the Bank of England identified.

There is no option that doesn’t make at least one of the three situations worse. The Bank of England’s report is a map of the terrain the Fed will navigate on April 28.

The Bank’s Financial Policy Committee noted that the conflict has made the global environment materially more unpredictable, and followed a period in which global risks were already elevated.

The Fed’s April meeting — with Powell leaving in May and Kevin Warsh waiting to take over — may be the most consequential central bank decision in a generation. And there is no good option on the menu.

What the Smart Money Is Doing Right Now

The institutional response to the Bank of England’s quarterly update has followed a consistent pattern across macro funds and family offices.

Shortening duration aggressively. Long-term government bonds are most exposed if yields spike in a disorderly unwind. The smart money is concentrated in short-term instruments — 3-month Treasury bills, money market funds, and very short-duration corporate paper — that mature quickly and can be redeployed if conditions change.

Exiting leveraged private credit exposure. The investors who understand the Bank of England’s comparison to 2008 are reducing their exposure to private credit funds that have used leverage to amplify returns in a low-rate environment. Those funds face the most severe stress in a higher-for-longer rate world with rising defaults.

Reducing concentration in AI infrastructure plays. The circular financing concern is generating quiet but real repositioning away from the companies most exposed to the AI capex cycle’s potential slowdown — particularly companies whose valuations assume sustained high levels of data center spending regardless of the interest rate environment.

Adding hard assets. Gold, silver, energy infrastructure, agricultural land — the assets that hold value in a world of simultaneous monetary and financial stress. The same thesis that has driven central bank gold buying at record pace for fifteen consecutive quarters continues to be validated by each new piece of macro data.

The One Thing the Bank of England Could Not Say

Central banks communicate carefully. They are institutional actors with legal obligations and market-moving authority. They cannot say everything they know. What they say publicly is less alarming than what they say in closed-door meetings with the Treasury and the prime minister.

What the Bank of England said publicly on April 1, 2026 was alarming enough. The chance of risks crystallizing simultaneously in government debt markets, private credit and AI valuations. Three separate crises. Potentially overlapping. In a materially more unpredictable global environment.

What the Bank of England could not say publicly — but what the data implies — is that the window for an orderly resolution of these risks is closing.

Every week that the Strait of Hormuz remains closed is a week that energy prices stay elevated. Every week that energy prices stay elevated is a week that inflation remains above the Fed’s target. Every week that inflation remains above target is a week that interest rates cannot be cut. Every week that interest rates cannot be cut is a week that private credit stress accumulates. Every week that private credit stress accumulates is a week that the AI financing cycle’s vulnerabilities grow.

The Bank of England drew the connection. It used the word simultaneously. It invoked the 2008 crisis by name.

The question is not whether these risks are real. The Bank of England is telling us they are.

The question is whether the people making monetary policy decisions in Washington, London, and Frankfurt can thread a needle that gets thinner every week the war continues.

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

where your money is leaking,

what to cut or renegotiate first,

how to protect your savings,

and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

This is not financial advice. Always consult a qualified financial advisor before making significant financial decisions. If this connected dots you hadn’t seen connected before — share it. And subscribe below for the next one.

At 6:49 a.m. on the morning of March 23, 2026, someone made a trade.

The oil market was tense. Brent crude was hovering near $100 per barrel. The Iran war had been running for 23 days. President Trump had spent the entire weekend threatening to bomb Iranian power plants unless Tehran reopened the Strait of Hormuz within 48 hours. The 48-hour ultimatum was expiring. Markets were bracing for escalation.

Nobody had any reason to believe the next 15 minutes would be anything other than more of the same.

And yet, between 6:49 a.m. and 6:50 a.m. — in a single 60-second window — approximately 6,200 Brent and West Texas Intermediate futures contracts changed hands. The notional value of those trades was $580 million. All of them positioned for oil prices to fall.

At 7:04 a.m., President Trump posted on Truth Social that the United States had been engaged in “productive conversations” with Iran toward “a complete and total resolution.” He ordered the Pentagon to pause all strikes on Iranian power plants.

Oil prices plummeted. Stock futures surged. Whoever held those positions profited enormously — potentially hundreds of millions of dollars — in the space of minutes.

The average trading volume for that same one-minute window over the previous five trading days: approximately 700 contracts.

On March 23, there were 6,200. Nearly nine times the average. In one minute. On a Monday morning with no scheduled economic data, no Fed speakers, no earnings reports — nothing that would normally generate that kind of volume.

“My gut from watching markets for the last 25 years is this is really abnormal,” an unnamed trader at a major hedge fund told the Financial Times. “It’s Monday morning, there’s no important data today, there aren’t any Fed speakers you’d want to front-run. It’s an unusually large trade for a day with no event risk.”

“Somebody,” the trader said, “just got a lot richer.”

The Evidence That Is Hard to Explain Away

The Financial Times broke the story. Bloomberg News confirmed the data. CBS News, NPR, The Guardian, Axios, and Fortune all independently verified the trading pattern. This is not one outlet reading suspicious patterns into noise. The data is documented, verified, and consistent across multiple independent analyses.

Here is what the evidence shows.

At 6:49:33 a.m. — 27 seconds before the full spike at 6:50 — trading volumes for Brent and WTI simultaneously jumped. This is not a gradual increase. It is a sudden, precise, coordinated spike that began at a specific moment with no public information available to explain it.

The oil futures trades positioned for prices to fall — which is precisely what happened after Trump’s post. Simultaneously, S&P 500 e-Mini futures traded on the Chicago Mercantile Exchange saw a sharp and isolated jump in volume, positioned for stocks to rise — which is also precisely what happened.

Both positions — short oil, long stocks — were exactly correct. Both moved in the profitable direction within minutes. Both trades occurred in a compressed window before any public information was available.

Bloomberg News analyzed trading in those markets during the same time period over the previous five days. The average level was around 700 contracts. In a single minute on March 23, 6,200 contracts were traded.

A position of roughly $580 million in futures exposure, established just minutes before Trump’s de-escalation post and liquidated after a $10-15 per barrel drop in oil prices, would yield profits easily in the hundreds of millions of dollars. A lawyer who specializes in futures trading told CBS News that “the massive spike in volume of trades right before that post is certainly enough to raise eyebrows, and I think to launch an investigation into what was behind that.”

What other explanation is there? “There was nothing else going on that would justify large transactions at that specific moment,” Nobel Prize-winning economist Paul Krugman told NPR.

The Prediction Market Evidence

The oil futures story is damning on its own. But the Financial Times investigation found a second, simultaneous pattern that is equally difficult to explain.

On the online prediction platform Polymarket — where users bet real money on real-world events — eight newly created accounts placed bets totaling approximately $70,000 on a US-Iran ceasefire. These accounts were created around March 21, two days before Trump’s announcement.

The Guardian reported that researchers found these accounts “definitely” showed signs of insider knowledge. Ben Yorke, an expert who analyzed the trading patterns, told The Guardian that the accounts “definitely” look like “someone with some degree of inside info.” The Guardian noted that “online crypto watchers and experts suggested that the bets bore the signs of insider trading — both because they bought their positions at market price, and because some of the accounts looked like they could belong to a single investor attempting to conceal their identity by splitting their bet between multiple wallets.”

According to Yorke: “Typically, when you see wallet-splitting and deliberate attempts to obfuscate identity, it’s one of two scenarios: either a very large investor trying to shield their position from market impact, or insider trading.”

If the Polymarket positions paid off on a ceasefire — which at $70,000 with prediction market leverage could yield approximately $820,000 — the oil futures trades generating potentially hundreds of millions of dollars dwarf them. But the Polymarket pattern reinforces the same conclusion: someone appears to have known what was coming.

The Pattern Before March 23

If March 23 were a single isolated incident, it could be dismissed. Strange things happen in markets. Coincidences occur.

But Axios reported a broader pattern that extends well beyond that single morning.

On the Friday before the Iran war began — February 27, 2026 — an unusual surge of more than 150 Polymarket accounts placed hundreds of bets predicting that the US would strike Iran. Those accounts bought their positions cheaply, before the odds reflected the true probability. When the strikes began the following day, those positions generated significant profits.

Six newly created Polymarket accounts in February had made approximately $1 million by correctly betting that the US would strike Iran by February 28, buying positions when the odds were still long.

Axios noted that Trump’s sons, Eric and Donald Jr., have invested in drone companies competing for Pentagon contracts. Jared Kushner — Trump’s son-in-law and one of his Iran envoys — was seeking to raise billions for his private equity fund from Persian Gulf governments entangled in the war.

The White House denied any wrongdoing. “The president has no involvement in business deals that would implicate his constitutional responsibilities,” White House counsel David Warrington told Axios.

But the pattern — across multiple markets, multiple events, multiple timeframes — is now too consistent to attribute to coincidence.

Why Paul Krugman Called It Treason

Paul Krugman is a Nobel Prize-winning economist who does not typically use the word “treason” casually. He used it on his Substack in response to the March 23 trading pattern.

“We have another word for situations in which people with access to confidential information regarding national security — such as plans to bomb or not to bomb another country — exploit that information for profit,” Krugman wrote. “That word is treason.”

His argument was not just moral. It was strategic.

Insider trading on national security decisions is illegal for reasons besides unfairness. Trading on classified information effectively broadcasts government plans to foreign adversaries. Krugman noted that if someone can infer classified military decisions from futures market movements — if an Iranian analyst is watching Brent crude futures and seeing unusual volume spikes 15 minutes before Trump’s Truth Social posts — the pattern itself becomes an intelligence leak.

“Who needs to bribe agents within the government,” he wrote, “when you can infer the same intelligence from futures markets?”

Iran’s parliament speaker, Mohammad-Bagher Ghalibaf, denied that any negotiations with Washington had taken place, calling the claim “fake news” used to “manipulate the financial and oil markets.” Whether or not that specific denial was accurate, the implication was pointed: someone in or near the US government appeared to be using geopolitical decisions to generate private market profits.

Krugman raised a question that has not been answered: “Are decisions about war and peace in part serving the cause of market manipulation rather than the national interest?”

What the CFTC Is Doing — And What It Isn’t

The Commodity Futures Trading Commission — the federal regulator responsible for overseeing futures markets — has the authority to investigate this.

A partner who specializes in futures trading at the law firm Troutman Pepper Locke told CBS News that the CFTC is “undergoing a sea-change right now because of this. They’re seeing more activity than they have seen in decades, maybe since they were created. They’re reassessing everything.”

The CFTC recently launched a proposed rulemaking process that focuses in part on what actions prediction markets should take to prevent insider trading. That process has implications not just for prediction exchanges, but for the oil futures markets where the most consequential activity appears to be occurring.

Congressional Democrats have said they are laying the groundwork for investigations into whether insiders are trading on Trump’s market-moving decisions. They are favored to win the House in November 2026, which means the investigation, if it happens, begins in January 2027 — long after the trades will have been cleared and profits distributed.

The CFTC has not publicly announced a formal investigation into the March 23 trading. The Department of Justice has not announced a criminal investigation. The Securities and Exchange Commission has not commented.

In the Martha Stewart insider trading case of 2004, federal prosecutors spent years pursuing someone who saved $45,000 by acting on a broker’s tip about a single stock. Stewart served five months in federal prison.

Whoever was behind the March 23 oil trades may have made hundreds of millions of dollars in less than 15 minutes, using information that could only have come from someone with advance knowledge of the President of the United States’ plans.

Nobody is in prison. Nobody has been publicly charged. Nobody has been named.

The Structural Problem This Exposes

The insider trading scandal — if that is what it is — exposes a structural vulnerability in the American system of governance that no investigation can fully address.

The President of the United States has the ability to move markets with a single social media post. That has been true since at least 2018, when Trump began using Twitter to comment on trade negotiations, Fed policy, and company-specific news in ways that generated measurable market movements.

What has changed is the magnitude. When oil is at $100 and the President’s posts can move it 10-15% in either direction — when a single social media post can redistribute tens of billions of dollars of value within minutes — the financial incentive to have advance knowledge of those posts is extraordinary.

The existing legal framework for preventing this exploitation was not designed for a world where the President communicates policy in real-time on social media, where algorithmic trading can execute $580 million in futures contracts in 60 seconds, where anonymous accounts on prediction markets can be created in minutes, and where the gap between the moment of decision and the moment of public announcement can be monetized with extraordinary precision.

The traditional insider trading framework requires a specific breach of a specific duty. The President of the United States is not a corporate insider in the legal sense. The rules designed to prevent corporate executives from trading on earnings announcements do not cleanly apply to situations where the market-moving information is a geopolitical decision.

The CFTC is reassessing. Congressional Democrats are building investigations. Lawyers are studying the question. All of that will take time. The trades have already been made.

What This Means for the Markets — And for Trust

Markets function on trust. Specifically, they function on the shared belief that prices reflect publicly available information — that no participant has an unfair advantage based on private access to decision-makers.

That belief is the foundation of market legitimacy. It is why retail investors participate. It is why pension funds hold equities. It is why ordinary Americans put their retirement savings in index funds that track prices set by markets they cannot see.

The March 23 trading pattern — regardless of whether it ultimately proves to be illegal, regardless of whether anyone is ever charged — has damaged that belief. Not fatally. Not irreversibly. But measurably.

A hedge fund trader who watched the volume spike told the Financial Times: “Somebody just got a lot richer.” That statement — from a professional market participant with 25 years of experience — is a recognition that the market’s integrity was compromised in that 60-second window.

The damage is not just to traders. It is to the system.

Martha Stewart saved $45,000 on a single trade and went to prison to make a point that no one is above the law.

Someone may have made hundreds of millions of dollars in 60 seconds on March 23, 2026, using information that was not available to anyone without access to the President’s plans.

The point has not yet been made.

Want to actually take action instead of just reading?

Most people understand what they should do with money — the problem is execution. That’s why I created The $1,000 Money Recovery Checklist.

It’s a simple, step-by-step checklist that shows you:

and how to start building your first $1,000 emergency fund without overwhelm.

where your money is leaking,

what to cut or renegotiate first,

how to protect your savings,

and how to start building your first $1,000 emergency fund without overwhelm.

No theory. No motivation talk. Just clear actions you can apply today.

If you want a practical next step after this article, click the button below and get instant access.

This is not financial advice. If this gave you a clearer picture of what may have happened on one of the most volatile mornings of 2026 — share it. The more people who understand how markets actually work — and who is profiting while they suffer — the harder it becomes to ignore. And subscribe below for the next one.

Scott Galloway walked on stage at South by Southwest two weeks ago and said something that no financial commentator is supposed to say out loud.

“At some point, we have to stop propping up the markets with young people’s credit cards.”

The audience — skewing young, skewing Gen Z — did not boo him.

They cheered.

That moment tells you everything you need to know about what is happening to the financial psychology of an entire generation. And what it means for markets, for monetary policy, and for the future of the American economy is something that Wall Street is only now beginning to reckon with.

The term is “financial nihilism.” It describes a generation that looked at the traditional playbook — save consistently, invest in the S&P 500, buy a house, build wealth slowly and patiently — and concluded, with remarkable clarity, that the playbook was written for a world that no longer exists.

And they are not wrong.

The Numbers That Explain Everything

Northwestern Mutual’s 2026 Planning & Progress Study — released earlier this month and based on 4,375 US adults surveyed between January 5 and 21 — produced findings that should be required reading for every policymaker, every central banker, and every financial institution that depends on the next generation participating in the conventional financial system.

Nearly one in three Gen Z adults are either using or considering high-risk financial tools — crypto, sports betting, prediction markets — as their primary wealth-building strategy.

Among Gen Z investors putting money into these assets, 80% said they believe such platforms offer a faster route to their goals than traditional methods. Not a slightly faster route. A fundamentally different route — one they have consciously chosen over the path their parents took.

42% of Gen Z investors hold crypto — nearly four times the 11% who hold a retirement account. Read that again. A 22-year-old in 2026 is four times more likely to own Bitcoin than to have an IRA.

80% of Gen Z respond that they feel left behind financially — with 75% of Millennials giving the same response.

32% of Gen Z and 24% of Millennials are currently invested in or considering prediction markets or sports betting sites in 2026.

These are not fringe behaviors. They are majority behaviors among the generation that is about to become the largest cohort in the American workforce and the dominant consumer of financial products for the next forty years.

Why This Is Rational, Not Reckless

Here is the argument that mainstream financial media keeps getting wrong.

Financial nihilism is consistently framed as irresponsible. As a failure of financial education. As young people making self-destructive decisions because they don’t understand compound interest or the long-term superiority of index fund investing.

That framing is condescending. And it misses the actual math.

Research from the University of Chicago and Northwestern University shows that as someone’s perceived probability of homeownership falls, their behavior often shifts — they consume more relative to their personal wealth and take a measurable turn toward riskier investments.

This is not irrationality. This is a rational response to a specific structural reality.

The traditional wealth-building playbook has three pillars: earn a stable income, save consistently, and invest in assets that compound over time. The most powerful of those assets, historically, has been a home. Buy a house young, build equity for thirty years, retire wealthy. That was the boomer path. That was the Gen X path. That path is gone for most of Gen Z.

The median US home price today requires a down payment that represents three to five years of after-tax income for the median Gen Z worker — assuming they save every dollar and spend nothing else. Mortgage rates at 6.5-7% make the monthly payment on a median home consume 40-50% of median household income. In major metropolitan areas, the math is simply impossible.

The significant increase in housing costs compared with previous generations makes home ownership unattainable for many Gen Z individuals. And when the primary on-ramp to compounding wealth — homeownership — is structurally inaccessible, the math of patient index fund investing changes fundamentally.

Here is the calculation a financially literate Gen Z person is actually making:

If I invest $500 per month in the S&P 500 starting at 25 — the traditional advice — and earn an average 8% annual return, I will have approximately $1.7 million at 65. Forty years of disciplined saving. A comfortable but not transformative retirement.

But I will never own a home in the city where my career exists. I will pay rent that inflates faster than my wages for forty years. I will watch asset owners — the people who already own real estate and stocks — compound their wealth at rates my savings cannot match. The K-shaped economy will widen the gap between me and them every single year, regardless of how disciplined I am.

Against that backdrop, the 22-year-old with $5,000 in crypto is not making an irrational bet. They are making a calculated decision that the expected value of a small chance at a large outcome exceeds the expected value of a certain path to a modest outcome in a system structurally stacked against them.

If the traditional system is structurally designed to enrich those who already own assets — and if every crash is backstopped before young buyers can get in at the bottom — then the conventional playbook isn’t just unappealing. It’s a trap.

That is the argument. It is coherent. And no amount of financial literacy campaigns will address it, because it is not a knowledge problem. It is a structural problem.

The $100 Trillion Crypto Derivatives Boom Nobody Is Explaining

Gen Z’s embrace of high-risk investments is a rational response to limited traditional wealth-building opportunities, such as affordable housing. And the scale of what they are building in response is staggering.

The crypto derivatives market — perpetual contracts, leveraged bets, options on digital assets — has crossed $100 trillion in annual volume in 2026. Not $100 billion. $100 trillion. A number larger than the entire global GDP.

The majority of that volume is driven by Gen Z and younger Millennials trading on platforms that didn’t exist five years ago, using financial instruments that their parents have never heard of, in markets that operate 24 hours a day, seven days a week, with no circuit breakers, no FDIC insurance, and no bailouts.

32% of Gen Z investors have exposure to prediction markets, and the cohort leads all generations in meme coin activity and usage of speculative platforms like Polymarket, favoring short-term, liquid markets over long-term holds.

Polymarket — the prediction market platform that allows users to bet on everything from election outcomes to whether a ceasefire will hold in the Middle East — has become one of the defining financial products of Gen Z. During the Iran crisis, Polymarket’s volumes on geopolitical events exceeded those of several major commodity exchanges. Young people are not just watching the news. They are betting on it, in real time, with real money.

Only 32% of Polymarket traders have turned any profit, with 92% of winners earning $1,000 or less.

The house wins. Almost always. The math is not different from a casino. But the casino is now framed as a financial instrument, accessible from a phone, designed to feel like informed analysis rather than gambling.

What Wall Street Actually Fears